| CATEGORII DOCUMENTE |

| Bulgara | Ceha slovaca | Croata | Engleza | Estona | Finlandeza | Franceza |

| Germana | Italiana | Letona | Lituaniana | Maghiara | Olandeza | Poloneza |

| Sarba | Slovena | Spaniola | Suedeza | Turca | Ucraineana |

Electronic Commerce Strategy

The aim of this review is to critically evaluate the term electronic commerce. It aims at taking into account frameworks and models associated with the term and their usefulness and expediency in todays rapidly changing business environment. This review reflects on models/frameworks of the recent past and the emergence of new qualifying models/framework within the wider literature. In evaluating their significance an attempt is made to present a more coherent and holistic understanding of e-commerce strategy.

Throughout the wider literature the impact of the Internet on industries, businesses and firms competitive advantage has been phenomenal. In that we have now entered a digital economy (Martin et al 2001), which is evolving rate and is expected to become a significant global economic element in the next century (Clinton and Gore 1997). E-commerce may be defined as the electronic transmission of buyer/seller transactions and other related info between individuals and businesses or between two or more businesses are trading partners (Martin et al 2001).

From the wider literature it has also become apparent of the importance of the term business model. Despite this increase in Internet usage and the need for business models there is a lack of appreciation about the central role that business models play in the face of the Internet and particularly the impact of the internet on business models and performance (Afuah, Allan 2001). The Internet stands to establish new game strategies; in which existing so- called brick and mortar strategies may become obsolete. For instance, Martin et al (1997) in his examination of strategic frameworks developed for a pre-Internet world cautioned that such frameworks may only be starting places for understanding e-commerce application opportunities via the Internet. For example Porters competitive forces model used for more than a decade for businesses to anticipate and plan strategic responses to five competitive forces (Porter 1985, Porter and Millar 1985), can provide a useful starting place for thinking about the commercial opportunities and threats introduced by the Internet. But may be limited by being a single industry model, where the internet and e-commerce comprehend the potential and need for a critical cross-industry consideration.

It has also become apparent that organisations are implementing models in a rather static form. In a sense, a quick fire strategy to gain a presence on the internet (Afush, Allan 2001, Nour et al 2001, Hackbath et al 2000). From the wider literature all readings highlight the dynamic ever changing nature associated with e-commerce, in that firms must initiate or respond to both exogenous and endogenous factors. Afuah, Allan (2001) stress the importance of this issue in their conceptualisation of a business model consisting of a system that is made up of components, linkages between the components and dynamics. These components and linkages do not last forever and therefore need to be continuously refined.

The need for continually refining models indicates that descriptive models may be very short-lived, in that rates of technological change are extremely fast (Nour et al 2000 and Hackbath et al 2000). Despite the models and frameworks presented in the wider literature describe or represent the organisation at a particular point in time and says nothing that would happen to the model in the face of change. Regardless of the fixed acquisition, many studies are further devalued in that they descriptive in nature and do not provide general guidelines for the commercial use of the web. Many models and frameworks do not account for differences in products, markets and companies and the impact these factors have on strategies being developed (Nour et al 2000). Therefore it may suggest that studies are limited by their focus on what is being done rather than what should be done. For instance Meyers (1997) put forward a model describing four ways a firm may use the internet, which include, as a new information channel, communication channel, distribution channel and transactional channel. Although it may provide some practicality into potential uses for the Internet, the model may be based on simplifying assumptions and may not be pragmatic when viewed from a customer or supplier perspective and limited in scope when examined in light of a different industry sector. For example the model becomes less distinct and useful when applied to the banking sector.

Therefore as the wider literature research points out there is a need for a normative model (Martin et al 2001;Nour et al 2001, Turban et al 2000) in that presents and identifies the best ways to take advantage of such an exciting electronic medium for achieving goals, creating competitive advantage, increasing market share and improving efficiency etc.

Despite the rather cavalier attitudes towards models, both in the past and present, the second part of this review will provide a decisive commentary on some of the key models and frameworks put forward in the popular media and provide a serious consideration of the usefulness, value and significance of models and frameworks that have appeared in the wider literature.

Mohamed. A. Nour and Adam Fadlalla (2000) proposed a conceptual classification model for virtual markets, and a framework for web-based marketing strategies. This is perhaps a more comprehensive model for e-commerce. The model/framework is useful in that it provides concrete web based marketing strategies to account for differences between products, such as the differences between products, such as the difference between goods and services, or between physical goods and information products. Therefore this strategic framework is explicitly useful from an e-commerce perspective.

Virtual markets Marketing functions Internet Tools

EPS Promotion Search/Retrieval

![]()

![]() ETS Selling Communications

ETS Selling Communications

DEM Delivery Modeling

DES Support Testing

![]()

![]()

![]()

The framework is further constructive in that the can provide web-based strategies irrespective of industry or product types, which can be based on unique characteristics of each of these markets. The framework is also useful in that it provides valuable web tools and technologies in supporting the various aspects of the marketing concept. Although the main critical aspect of the model is that e-commerce or the webs role may be limited, in delivering the components of the marketing function. In that no matter how much technology progress, it will never be possible to deliver a car by the web (Begin, L; Boisvert H 2002). The model also proposes strategies for selling or payment strategies, although from the wider literature there is a growing body of research suggesting that electronic commerce has been limited by lack of a secure Internet payment infrastructure (Crede, 1995; Good J, Schultz 2002). Despite the framework emphasising that it enables an organisation to determine its web strategy based on its associated quadrant, there is a growth of literature suggesting that strategies are becoming difficult and vary due to the vary wide based spectrum of issue associated with the internet (Higgins and Hogan, 1999).

In spite of these drawbacks the framework presented can be used by companies to which Web-enabled market they belong to, which web marketing strategies to launch, which web tools to use and how to launch these strategies.

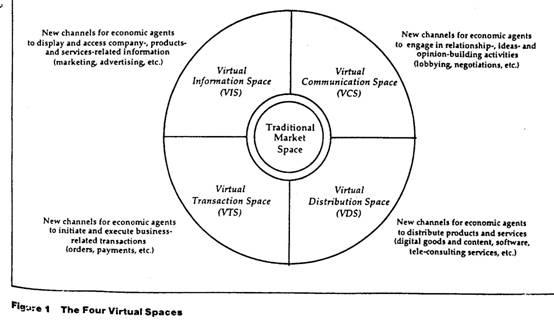

Albert Angehrn (1997) proposed a ICDT model, which is used as a systematic framework for guiding the analysis of how traditional products and services are redesigned in the light of the internet and the identification of organisational adjustments companies need to undergo in order to fully exploit the opportunities created by the internet. This framework is useful in that it segments business opportunities created by the Internet into four virtual spaces; a virtual information space, a virtual communication space, virtual distribution space and a virtual transaction space.

Figure 2- The Four virtual space model

![]()

The framework is not also useful by distinguishing between these types of internet presence but also provides valuable commentary in that each type can be classified in terms of its technical sophistication and the level of customisation (from generic to custom-tailored distribution). The model therefore allows for a systematic analysis. For instance, if they have established a simple or generic presence. The framework also allows of the analysing the impact of the Internet on the evolution and extension of the market offer, which may provide greater clarity as suggested by Afuah and Allan (2001) many models take a narrow view and do not assess the impact of internet technology. The ICDT Model also indicates explicitly the emergence of a new, potentially important market space, the Virtual Communication Space (VCS). Although despite the framework emphasising the importance of (VCS) there is still limited understanding of this environment.

Gary Hackbarth and William J. Kettinger (2000) discussed the three levels of E-business and then introduced a strategic E-breakout methodology that helps an enterprise to transform itself to Level 3- E- business Transformation. This framework is particularly useful in that it charts E-business strategies passing through three levels of increasing sophistication. From level 1 (Experimentation), level 2 (Integration) to level 3 (transformation). Becoming a Level 3 company symbolises the transformed businesses of the twenty-first century. In that organisations must continually respond to strategic threats and capitalise on market opportunities (Begin and Boisvert 2002), which is the essence of the strategic E-breakout methodology. Therefore this framework is adoptive in the sense it considers the dynamic or evolving nature of models, recognised by Afuah and Allan (2001) and can be applied to a customer, supplier and competitor perspective (Silverstein, 1999; Wymbs, 2000)

The framework also develops an understanding of the use of eTouch Points, which potentially reveal opportunities, and threats for effective application of E-business technology. Touch-points can be used to examine the linkages and can then be improved and possibly redesigned, with E-business technologies.

The strategic E-breakout methodology is useful in its application of assisting companies to rethink its corporate strategy to maximise its E-business strategy. Therefore this may be a more comprehensive model in that it not only helps organisations to develop a potential strategy but also maximise or to capitalise on strategic development, which is needed in the rapidly changing environment (Varadarajan and Jayachandrian, 1999). The strategic breakout methodology sequentially follows four logical stages: initiate, diagnose, breakout and transition.

This framework is extremely useful in allowing strategic e-commerce development in todays robust and dynamic environment. The model makes every effort to understand the various relations of the organisation. For instance customers and suppliers prior to implementing the strategy. In examining the value chain alternative technologies can be comprehended, in which may forward the company ahead of its competitors and influence the direction of the company, which is needed in todays competitive environment.

Marshall and McKay (2002) propose a holistic and integrated framework for planning the adaptation and implementation of electronic commerce (EC). The researchers used the framework to formulate questions to guide the CEO in thinking about appropriate strategies and initiatives for e-business. This model is perhaps useful in that it is expected that management teams, could navigate their way through this framework without external support. The framework recognises that thinking about e-business strategy is often incomplete, that there were gaps in the ideas of management, resulting in incompleteness and difficulties when the strategy was implemented. The aim of the model was to remedy that situation, in providing a relatively transparent approach to e-business strategy formulation which would attempt to guide and trigger thinking about e-business and questions in areas vital to e-business success.

By offering an integrated, holistic framework the framework is useful in that it encourages a more systematic consideration of a more complete range of issues, in particular, structuring their thoughts about EC issues pertinent to their particular business and industries. In the wider literature is often suggested that management are poorly equipped to assess the advice of consultants (Deise, M. V, Nowikow, C, King.P. and Wright 2000). In that they felt unsure how to evaluate the recommendations made by consultants. Allow further investigation would need to ascertain whether the framework would serve more generally as a device to evaluate e-business initiatives.

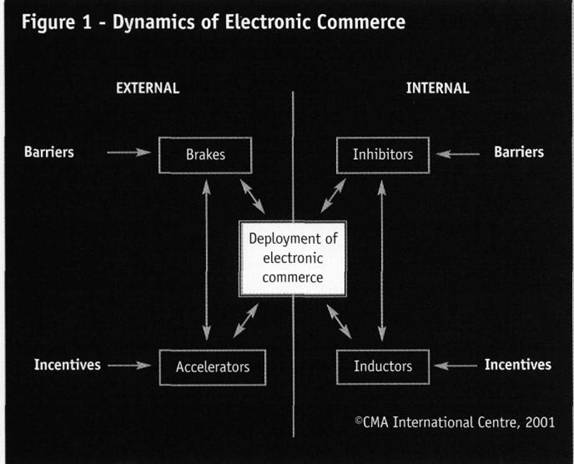

Begin and Boisvert (2002) suggest that when developing an e-commerce strategy, SWOT analysis should be complemented by a framework, which they have called Dynamics of electronic commerce. In their words the model differentiates barriers and incentives by whether the companies can act on the factors in questions.

For the model to work efficiently, it is recommended that companies concentrate on the internal factors which they have control over i.e. Inhibitors and Inductors and avoid focusing on factors it cannot influence, for instance brakes and accelerators.

In this framework accelerators and inductors are seen as incentives to development of an Internet presence while brakes and inhibitors are seen as barriers to this. In order for an e-commerce strategy to be successful these opposing factors must be managed carefully.

So in conclusion I vacillate to develop a model or framework that capture all of the above mentioned. There may some debate as to the critically value of a framework. Although having said this, models and frameworks do provide valuable insights and perspectives when developing an e-commerce strategy, in which they guide the organisation in developing and implementing a strategy critical for todays evolving environment. Although what may be critical is the understanding of a framework from a dynamic perspective and the involvement of organisational partners, such as customers and suppliers. The ever changing nature of e-commerce may result in e-strategy having a transitory dimension. Therefore it requires constant on-gong attention, improvements and refocusing of e-commerce strategies.

The Banking sector is a long established

industry sector on which all other sectors rely. Modern banking is thought to date back to

The twentieth century saw massive leaps in the way banking was conducted due to a rapidly increasing marketplace. Vast improvements in transport and communication links mean banking now faces worldwide competition, opportunities and also threats. This has led to the need to compete effectively in the global markets and one way to do that is through the ever-growing opportunity of the Internet

The Internet is now engulfing the market for personal banking services, which began with the arrival of the telephone banking and the development of call centres. All the major retail banks are aggressively promoting Internet banking. Some are using the Internet as one of many distribution channels for a variety of products and services; others have created new Internet only banks, thereby taking advantage of lower market entry cost to capture new customers and to gain an early share of the very large personal banking market.

In 2000, the market was worth an estimated 159.8bn at current prices, and over the next five years the volume of business for personal banking is anticipated to increase by 13.7%, to reach 189.7bn by the end of 2005.

E-commerce strategy has really started to affect banks since the development of secure sites and the establishment of customer confidence in the measures being taken. Previously it had been sufficient to post investor-related data online to satisfy the then quite small, but ever increasing Internet community. Now users want access to banking services anywhere and anytime and are also offered a cheaper and wider range of services by Internet Banking Professor Feng Li Of Newcastle University (Sept 2002). Traditional banks have no choice but to adapt and to do so rapidly.

PC banking and more recently, Internet

banking, allow customers instant and direct access to their accounts. The Royal Bank of

According to the Regional Review of Northern Ireland now is a good time for companies in NI to expand and branch out as a period of relative stability (with reference to the political situation) ushers in a more confident business environment (www.icclaw.com/l500/edit/ni2.htm).

The Internet is revolutionising personal banking. Its strongest advocates claim that it will bring freedom to personal bank customers and give them complete control of their finances at the touch of a button. Internet banking is available 24hr a day from anywhere in the world. With Internet access becoming available via keyboards attached to digital television, via palm-help computers and WAP (Wireless Application Protocol), it is clear that service providers are keen to offer customers many points of access to systems that are designed to help them organise their personal finance.

Internet banking requires an e-commerce strategy that seeks to improve services and tighten the relationship with customers. Internet banking can have a positive effect on this strategy, as it should decrease paperwork and queues at high street branches. There can also be negative impacts including depersonalisation of service that can lead to customers feeling unimportant. Different banks deal with this in different ways through their e-commerce strategy. This project seeks to compare and contrast several banks strategies in order to recognise different approaches.

BANK OF

The Bank of Ireland website www.bankofireland.co.uk was chosen as it is a well-known bank in this province. It provides online access for holders of personal accounts as well as the business sector.

Banking 365 allows personal account users access to their accounts via telephone or Internet 24 hours a day all year round. The company uses high-level security techniques, for worry free e banking. The services include transferring funds between accounts, balance enquiries, ordering chequebooks and statements as well as pay bills. This should improve customer service for those people using the high street branches by cutting down on unnecessary visits to the bank, which will in turn shorten queues. This is good business sense as an aim of e-commerce strategy is to tighten links with customers and improve customer service.

Business on Line is the business-focused side of Bank of Irelands online services. This is available for businesses to work in conjunction with telephone and traditional banking and is available 24 hours a day, all year round. It offers services including making payments from accounts, paying employees and also allows interaction with Customer Support Team as well as Banking 365 services. It also offers three levels of service depending on the type of company and what services they require.

The group believed the Bank of Ireland would be of interest to compare its successfulness with the other banks to see if providing services to two different sectors of the market (personal and business e banking) at once was too ambitious to begin with.

One bank chosen in the Banking sector is

the

www.halifax.co.uk OR www.halifaxonline.co.uk

We chose Intelligent Finance (IF) because it is an example of a successful bank, which has no high street branches. Also some of the group members have accounts with IF which gave us an insight into how their business operates. Their web address is www.if.com

BANK OF

The Bank of Ireland has developed an e-commerce strategy that seeks to improve customer focus and decrease costs to the company. In relation to Hackbarth and Kettinger (2000) the Bank of Ireland have reached Level Two in the three levels of e-business, as they are directly supporting current business strategies e.g. business and personal banking. Level Two can also be identified in that The Bank of Ireland are trying to cut costs by using e-technology and provide a superior service to customers in order to promote life long banking Ken Dobbin e-commerce Manager. According to www.abacus-e.com/strat.htm the frontline of e-business is the race to win and keep customers and this is what the Bank of Ireland are actively seeking to do.

When developing any strategy to implement

e-commerce it is important to have a structure to guide management and ensure

no holes are left in the ideas. Management can achieve this by using

The Bank of Ireland e-commerce management team realised the need to develop an advantage to at least stop a disadvantage by tempting people to use the site. One method of doing this is to offer cheaper transaction costs and those offered by the Bank of Ireland are significantly so e.g. a manual transaction would cost 52 pence whereas the same transaction online would cost 12 pence. As a group we feel this would attract many businesses join the Bank of Ireland as their running costs could be lowered so making them more efficient. The age of the Internet and e-commerce has had a huge effect upon the way in which, we both live and work. www.abacus-e.com/strat.htm. This is a good strategy for promotion but is used by other banks so different elements should be developed by the Bank of Ireland to ensure competitive advantage.

Ken Dobbin revealed that the company was more than happy with the performance of the Website so far. Banking 365 Telephone was the most popular of the services with 320,000 active users completing 8 million calls, which was a 60% increase on last year. Banking 365 Online has currently 200,000 users and completed 4 million transactions online, which was a 75% increase on last year. Mr Dobbin commented that it had been a worthwhile venture and that further development and marketing would mean it would fast become a vital part of the Banks everyday business.

The Bank of Ireland e-commerce strategy fits into the Information, Communication, Distribution, Transaction Model (ICDT) in the Virtual Distribution Space (VDS). The management have sought to decrease cost yet improve quality by distributing their service via the Internet. They offer customers lots of support online via email, 24-hour customer service and business customer training to use the new online banking as well as constant updates online about accounts.

The Bank of Ireland were very aware that past bad press coverage of security breaches would discourage consumers from using their services. It worked actively to ensure customer trust had been regained as on the website, in leaflets given out and in the interview the level of security was stressed. The measures taken were, therefore, also for the peace of mind of customers as well as providing a safe banking environment. The Bank of Ireland could therefore be said to be verging on the Virtual Transaction Space (VTS) in the ICDT model as it offers secure methods of payment online (explained below).

In order to secure personal details, they

used the strongest commercially available technologies. These included unique passwords, changed

every month, digital certificates for those making payments from accounts e.g.

businesses paying employees and encryption to scramble all data moving to and

from the bank and its customers. This

technology was so advanced that its export from the

The confidence created in customers by the security of the site reflects the idea of Touch Points in the Customer/Supplier Life Cycle that hopes to strengthen the relationship with customers Hackbarth and Kettinger (2000). In the last year alone usage, satisfaction levels and sales increased strongly Preliniary Annual Report (2002).

The Bank of Ireland website also offers a Virtual Information Space as it offers a wide range of information about themselves and the services they provide (www.bankofireland.co.uk). They do however escape the brochure syndrome aspect of this as they have developed the VTS side of the site and offer security and distribution of their services e.g. Banking 365 and Business Online. The group feel that competition from rival banks has encouraged the Bank of Ireland to strive towards higher levels of services even though the bank is quite well advanced.

The advantages gained through e banking can be lost through customers seeing the service as impersonal. The Bank of Ireland showed its awareness of adding Touch Points to the service which, will increase customer trust, confidence and loyalty Hackbarth and Kettinger (2000). These include training of business customers staff to use Business Online, installation of Internet Explorer in businesses needing it, the many points of contact (Online, Telephone and Branches) as well as customer service 365 days a year. Ken Dobbin explains the strategy well when he says that simple touch points can really make a difference to customer choice and we want to sway them in our direction. The preliminary annual report 2002 illustrated how the Bank of Ireland had gained a clear market advantage from the quality of the electronic banking services and the application of customer relationship management principles facilitated by technology.

Online services need to be marketed in the correct way and the market a company is in will affect its e-commerce strategy. The Bank of Ireland Online service is in the enviable position of being in the Electronic Publishing and Software position (EPS) Nour and Fadlalla (2000). It does however still rely on its high street branches and so is by no means as well developed, as e-banks like IF. This type of marketing can take place online and creates product awareness through basic information available on the site. To publicise what the services can do for personal and business banking the Bank of Ireland offer a demonstration of the functional characteristics of both Business Online and Banking 365 Nour and Fadlalla (2000). The Bank of Ireland offers great customer support as they see this as a vital Touch Point. They use strategies like email contact if customers have complaints, 24-hour customer service for problems and reassurances and also feedback forms which are used to improve the services constantly.

Looking at the Internal part of the strategy offered by Marshall and McKay (2002) the Bank of Ireland invested heavily in IT in order obtain the best security. They were eager that the online facility would improve customer relationship management and this was ensured through 24-hour customer service, the many points of contact and the provision of secure Electronic Funds Transfer.

According to Angehrn and Meyer (1997) the Bank of Ireland offers primarily a communication channel as it allows customers to interact with the bank to gain information on accounts, and lets customer interact with employees via email and call centres. It is also a transaction channel as payment to employees and suppliers can be made by businesses. Finally it may be considered as an information channel as browsing customers both potential and existing can view information on services available and the company itself.

Ken Dobbin claimed that Business On Line was a unique service as the needs of each business are assessed and a particular level of service is offered. Level one offers real time access to account information. Level two offers facilities to help businesses involved in International Trade. Finally Level three meets the sophisticated requirements of the corporate customer. On further investigation this strategy was developed when trying to decide how to cater for so many different business sizes and needs. This mirrors the Breakout stage in the Strategic E-Breakout Methodology developed by Hackbarth and Kettinger (2000). In this stage business strategies are aligned with SWOT analysiss to minimise weaknesses and often new, better strategies are formulated. This strategy means the customer base remains wide even though the service is provided on the Internet, as the customer does not have to be present to receive the information.

The e-commerce strategy for the Bank of Ireland appears to be well linked to its corporate strategy and would suggest a keen interest in looking after customers. It would be correct to state that the Bank of Ireland would have benefited from using the Marshall and McKay framework more fully. A better analysis of the Market and overall environment may have allowed them to make better informed judgements, but the group feel that the company offer good facilities to all its customers and are keen to improve and add to their portfolio of services. With the investment in online user points in larger branches Ken Dobbin hopes the uptake of the Online and telephone services will increase even more rapidly in the future.

The address www.halifaxonline.co.uk takes

you to the website where you are able to log into your accounts, view your

portfolio and use the services. When logging

onto the site you have to answer three questions as a security measure. The first two are quite standard being the

username and password and the third is a personal question, which changes each

time you go to log in. In the past,

e-commerce was limited by the lack of a secure Internet payment

infrastructure Crede 1995. The measures

taken by

The

The Halifax Group PLC has reached Level Two in the three levels of business developed by Hackbarth and Kettinger (2000) as they have integrated personal banking facilities in the high street branches into their e-commerce strategy. Their website poses a serious threat to competitors as it offers all the services of a high street branch round the clock without any queues and inconvenience. They seek to provide better value for both customers and their own company and have achieved this through cost savings made possible by attractive rates of online (see web saver (www.halifax.co.uk/savings) for details). The Halifax Group PLCs core business was mortgages and savings but this has been identified as a type of weakness. This echos the reviewing that takes place in companies at Level Two in order to find opportunities to be seized.

Initially, Halifax Online offered share

dealing and banking facilities but has expanded considerably. The range of Internet services available, via

the unique 'portfolio' view, now includes savings, sharesave,

household insurance, mortgage promise, mortgage enquirer, Travel Money

ordering, online applications for current account, personal loans, credit card

and travel insurance. This proves the

Halifax Group PLC strategy is to be the

leading provider of personal financial services in the

However since that observation 2 years ago

the

Judging by their five-year summary of their

financial accounts they are growing greatly and their profits have increased

dramatically. They have established

themselves as the fastest growing bank and credit brands with 22% of new

accounts and 25% of new cards being taken up by the

Since launching in October 1999, Halifax Online has been attracting new users at the rate of over 1,200 per day and to achieve this they have obviously marketed themselves effectively online Nour and Fadlalla (2000). One way they have done this is by using prize draw competitions as part of their strategy to encourage customers to open a Halifax Web Saver account. Between 26th August and 31st October 2002 those choosing to open such an account were entered into a prize draw. Ten winners each received 2,000 credited to their Web Saver accounts. This shows good strategy preparation on the part of the e-commerce team as they are using their site for many purposes e.g. as a transaction channel, an information channel (information on their company and services) and also a communication channel as they use these prize draws to get customers and gather information about them.

The company is now seeing transaction volumes on the scale of 190,000 external transfers performed per month and statement pages viewed at over 600,000. The wide range of products and services available through Halifax Online have proved popular, over 75% of Halifax Online users have two or more products. Around 70% of online customers use the service to manage their current account, and since its launch, in April 2000, over 300,000 Web Saver accounts have been opened.

The

Commenting, Paul Waggott, Head of E-Commerce, Halifax said,

'These figures show customers are increasingly inclined to use our online services and take advantage of the convenience and time saving the service offers.(See KEYNOTES Market Report 2000, Personal Banking, Eleventh Edition 2000, Edited by Jenny Baxter)

It may have been advantageous for the

Within the structure of the organisation the

Bank of Ireland managed their customer relationship by offering demonstrations

and help lines. They took active steps

to involve all customers in their new facilities by investing in IT to provide

e banking in over 600 stores and good security online. The group feels that the

Launched

in July 2000 IF aimed to become successful by offering what customers

increasingly demand- choice and flexibility with cutting edge technology (IF

press release, 18/2/2000). They envisaged doing this by setting up the

Although

they offer telephone banking, it is the e-commerce aspect which IF wish to promote and it is this method by which they see

their company operating in the long term. As Heather Scott, Corporate

Communications Manager at IF, commented in an e-mail

to us- We do not believe that the

That said, Ms. Scott also commented that of the 50% [of customers] who apply by phone, over 60% of them migrate to the web once their account is opened. This means that IF are conducting over 80% of their business online.

In

order to be successful using an e-commerce strategy, Angehrn (1997) insists

that companies need to follow the ICDT Model. Within this, they will need to

think about which strategy to use, either the Virtual

Information Space (VIS), Virtual Communications Space (VCS), Virtual

Transaction Space (VTS) or the Virtual Distribution Space (VDS) strategy. When

writing this paper Angehrn mentions a recent report that shows that the banking

sector mainly concentrated on using the Internet as a

When applying this model to IF we felt that the emphasis had changed. We believe this is because the banking sector have now realised the potential of the Internet to carry out their business as opposed to simply informing the public about their business and directing them to their nearest high street branch.

From

IFs point of view, we believe that they now concentrate on the Internet as a

VTS as this is how they can grow their business and become more successful. As

well as this, however, their website does show evidence of all of the other

aspects of this model being used. By including pages such as

How it Works and About Us IF are displaying aspects of the

For the above reasons we believe, whether they are aware of it or not, IF are following Angehrns Model of how to design Mature Internet Business Strategies very closely and are probably following the VTS strategy approach but as mentioned by Nour and Fadlalla (2000) when commenting on Angehrns Model [these] four web usesare not necessarily distinct. As an alternative Nour and Fadlalla (2000) suggest a different model for Web strategies which they call A Conceptual Model for Internet-Based Virtual Markets. This model includes four quadrants labelled Electronic and Publishing Software (EPS), Electronic Tele-Services (ETS), Digitally-Enabled Merchandising (DEM) and Digitally- Enabled Services (DES). By virtue of the fact that IF provide a service and that transactions within this service can be completed electronically, IF are placed in the ETS quadrant. Companies in this quadrant are most suited to the Internet and as Nour and Fadlalla (2000) comment- all the marketing functions and activities in this market lend themselves to Internet automation.

Although financial services seem like the ideal sector to take advantage of the potential of the Internet when following Nour and Fadlallas model, Heather Scott- Corporate Communications Manager at IF, does not believe the Internet can replace high street outlets completely. When asked Can you envisage a time when telenet financial services organisations effectively replace traditional High Street outlets?, she replied No- there will always be a place for High Street banks. However, customers may have to get used to paying for service- likely by way of less keen rates. This, we believe, shows that even highly ranked employees of Internet (telenet) banks believe their companies are simply add-ons to complement the traditional banking sector and will never become the only method of banking.

Another paper which we consulted was entitled Building an E-business Strategy and was written by Hackbarth and Kettinger (2000). This outlined a number of frameworks for businesses to follow to make the most of their Internet presence. One of these was the Strategic e-Breakout Methodology and was split into four sections: - initiate, diagnose, breakout and transition. This methodology is intended for companies new to the Internet or wishing to make their Internet presence more effective. Although they are the best performing direct bank (IF press release, 26/7/2002), IF could still benefit by consulting such a methodology.

With the increase in use of the Internet in recent years it seems that IF have entered the market at the right time. As mentioned earlier, IF was launched in July 2000. By November 2000 they were opening, on average, over one account per minute (IF press release, 30/11/2000). This rise has continued and by July 2002 IF had passed the 500,000 mark for accounts. Cynics may say that people open these accounts but rarely use them, however, in the first half-year to June 2002, IF boasted assets and liabilities in excess of 12 billion.

When thinking about a telenet bank, the group felt that the greatest attraction of them to customers would be that they are available at any time. Heather Scott agree with this but also pinpointed the fact that IFs customers have more control over their banking since you can see every day/hour/weekexactly where your money is going.

We felt that the perceived lack of security of Internet banking may be the main reason why people choose not to bank in this way however, on this point, we were proved wrong. Heather Scott insists that although security was a problem when IF was launched, people now realise that a robber could call into their local branch with a stocking over their head. IF are so confident about this that they offer an online guarantee that anyone subject to fraud will be reimbursed by them.

In conclusion to this section, it seems that although the Internet and Internet banking are becoming more popular and making plenty of money for their owners, those in influential positions within all types of banks believe traditional banking has a part to play in the future of financial services.

customers will still want bricks as well as clicks. (John

Stewart, Chief Executive of Woolwich, cited by

|

Bank of |

Intelligent Finance (IF) |

|

Costs to bank |

Higher costs than an internet only bank but lower than a traditional offline bank |

Higher costs than an internet only bank but lower than a traditional offline bank |

Purely internet based means costs of roughly half that of traditional offline banks |

|

Usability of website |

Easy to navigate and offers many features. |

We found it hard to find information. However many features are offered |

Easy to navigate and very simple to use. Some features exclusive to the internet. |

|

Hours of business |

The only one that truly offers all banking service 24/7 |

||

|

Customer support online |

Demonstrations online and can be contacted via email/telephone. |

Excellent. Can be contacted via email.24 hrs customer service phone lines and demonstrations online |

Excellent as 80% of business is carried out online. Has email/telephone etc all open to the customer 24/7 |

|

Security features online |

Asked for user name and password. Also a series of questions one of which is asked every time you attempt to go online. Also provide a guarantee to reimburse against fraudulent activity. |

Pin number, which is changed every month. Software is installed on users hard disk to enable transactions to occur only from certain computers. |

Asked for user name and password. Also a series of questions one of which is asked every time you attempt to go online. Also provide a guarantee to reimburse against fraudulent activity. There spoke persons boast this site cannot be hacked into |

|

Firewall present at this site? |

yes |

yes |

yes |

|

Distribution channel |

Internet/telephone/branches/ mobiles and ATM |

Internet/telephone/branches and ATM |

Internet/Telephone/mobile |

|

Reach of services |

Wide reach because customer have a choice of distribution channels |

Wide reach because customer have a choice of distribution channels |

Excludes all those who do not have internet access or access to a telephone, feel intimidated by this technological progression |

|

Proportion of customers that use internet services |

Internet

usage is rapidly increasing for |

Quite low. Most Bank of Ireland customers use traditional banking methods. We feel this is because they are generally an older clientele and are resistant to change. |

Very high. Heather Scott (Corporate communications manager) estimates this too be approx 80%. |

|

Customisation of website |

Straight forward with no real attempt to customise for the individual. However all things are catered for. Its just a matter of trying to find them. |

Tailored business packages-only paying for the services you use. |

Highly customised services as they realise this is the way to obtain a competitive advantage. |

|

Aesthetics of website |

Limited use of interface. |

Graphical and colourful interface. |

Good interface, graphics and easy to read. |

|

Internet only or clicks and mortar |

Clicks and mortar |

Clicks and mortar |

Internet only |

AdvertisingHypertext Animation Audio Intelligent system |

Yes No No No |

Yes No No No |

Yes (More user friendly) Yes Yes Yes |

The Banks have both similarities and differences that will be explored in this section. The pure Internet bank IF has advantages over the others in regards to costs and so on. However, drawbacks can also be identified such as the discrimination against groups of consumers not online. The comparisons and contrasts of the chosen companies e-commerce strategy will now be discussed more fully.

All three banks have transactional websites where customers can use the services 24 hours a day, seven days a week. For the Halifax and Bank of Ireland this means more access for customers than traditional banking as their customers have more time to complete transactions when it is convenient for them. In this way these banks are using the Web to improve customer service and retention of customers

It is important for these banks to have attractive and easy to manoeuvre websites in order to keep customers and attract new ones. From the three banks studied IF seems to offer the most usable site with simple links to get to the important services. If offers more user friendly hypertext and animation and audio to improve the appeal of the site to customers.

For a more traditional bank

Internet banking offers cost savings for both the Banks and their customers. IF is a purely Internet Bank and so has lower overheads as there are no branches to maintain and less employees. The transaction costs are lowered due to this and so it is a great way for IF to win customers. This company is using the advantage of the Web to create a competitive advantage for its company. The Halifax and Bank of Ireland have online services and so are saving money on day-to-day running costs such as less paperwork, manual processing and mailing of brochure type information. These savings are reflected in lower transaction costs online, which these banks hope, will encourage customers to bank with them. It is true to state that IF will experience more savings and so be able to grant lower costs for customers.

Security is one of the biggest issues facing

e banking today. Many people are seeking backup from traditional banks in an

attempt to get a promise of security. IF

offers the capacity to bank using the telephone but unless customers are

confident about security measures they may still be hesitant. The

A possible disadvantage of IF the pure Internet bank could be its totally digital distribution channel. Although it is making complete use of all the benefits to be conferred by the Internet it is losing out on customers who are not online. In this case the Bank of Ireland and the Halifax are at an advantage as they are able to take advantage of lower costs of being online and yet have traditional banking services e.g. telephone, face to face and ATMs to reach the other section of the customer base. The Bank of Ireland and Halifax could be seen as taking the advantages of e-commerce and traditional banking to increase profits for themselves and provide a more complete service for their customers.

The proportion of customers using the web

facilities offered by these banks varies greatly with Heather Scott estimating

that up to 80% of customers use the Web to bank with IF. This means that costs for IF would be at a

minimum and so they are able to use the web to maximise their profits and

create a better service for their customers. The proportion of customers using the online services at

Personalised contact with the customers is of vital importance, as online services can feel impersonal to customers. There are ways to overcome this by using web-based technologies for customer support. IF carries out demonstrations online, of the services they offer, and can be contacted by email if problems do arise. They also provide back up via telephone for those not wanting to bank online. By using these web-based technologies for customer support IF can enlarge its customer base and use the information gathered from customers to improve the service for the future.

The Halifax and the Bank of Ireland provide many points of contact for customer interaction including email, telephone and online demonstrations. The Bank of Ireland provides a 24 hour customer help line which is open every day of the year. The Bank of Irelands main aim for using e banking is to improve customer service and they are using the advantages made possible by the Internet to improve the service. The Halifax and IFs aim is also to improve customer service but also to make a financial difference to their company so in this way all the companies are succeeding. Perhaps the Bank of Ireland needs to take better advantage of the cost and marketing benefits and to be gained via the Internet.

Customisation of the website will also lead

to a feeling of personalisation for the customer. Again the pure Internet bank IF provided

highly customised services as they realise this is the way to gain competitive

advantage over the other banks. The

In conclusion the pure Internet bank IF appears to have taken advantage of the potential benefits of the web. It has taken account of the gains to be made by catering for customer needs. It has taken advantage of the lower costs of running a bank online (lower overheads) and has used this advantage to improve its site both functionally and aesthetically. Both have encouraged more users as it means customers get what they need and get it quickly and easily.

The other more traditional banks have taken

some of the advantages provided by the Internet to improve their service. These are steps in the right direction toward

true e banking but fall short of the true Internet Banking ideal. The

It has been realised recently that banks can gain substantial benefits from providing Internet services. Through the years the industry has progressed from the primitive basic web pages to one today such as www.if.com where everything can be done online, a truly sophisticated transactional site. On this site you can set up direct debits, pay bills, transfer money and even apply for loans and credit cards with a decision back in minutes. This obviously is a great advantage to this bank. From the wider literature these technologies must be adopted to capture true Internet protection. Failure to adopt these current practices now will result in clear disadvantage. (Malcolm 2001).

The protection incumbent banks once had in

the 1950s-1980s from any form of external competition has now come to an end,

in the

In 1999 there were 2.8 million active

online banking users. This is predicted to rise to over 6 million in 2003. This

represents a growth of some 30% each year. Currently over 75% of all banks in

If we look at all forms of electronic banking, which includes ATM and tele-banking, in 1999 there were 63 million contacts between customer and bank. This figure is expected to rise to 78 million by 2003. This can be done by fostering the customers loyalty and really appealing to new customers. The old adage goes people are statistically more likely to divorce than change bank however, e-commerce allows more easy comparisons between banks and so customer migration may well increase if online banking becomes the standard and some banks get left behind when predicting changes in this new sector.

Ghani (2001) predicts that by the year

2003, the number of people accessing personal account information online will

grow to 40 million -- five times the 1998 rate. And the gap between wireless

and landline users is narrowing fast. 100 million

Forrester (2002) estimates that financial services on electronic channels (or financial e-business for short) will amount to USD 80 billion by the year 2003, up from about USD 14 billion today. But Forrester Research also said that this would be only six percent of the total value of business driven through electronic commerce at that time, in other words, a part of but not wholly a dominant part of the whole. Therefore from the wider research there is expected to a dramatic increase in the use of e banking.

The critics of Internet banks are very sceptical. They argue it all depends on how fast they can grow their deposit bases. Ernst and Young suggested there is a finite market segment of people who want to accept goods and services in a virtual manner. However in their defence its clear that the internet only banks are aware of this as they admit the advantage of traditional banks by brand name and image but we deal with this by providing an excellent level of service with great value.(Grimes 2002)

Another line of critics say that the click and brick banks will win in the near future as they have an image and therefore can migrate their customers onto the Internet through time. For this to work, however, companies must be willing to let their old distribution channels be cannibalised by their new ones i.e. let their new business take customers away from their traditional one (Mols, 2001).

Many theorists seem to think that banks will combine services to offer a vast range of products to the customer in the not so distant future. For example, if you apply online for a car loan they will ask you about insurance details and give you an automatic quote for insuring your new car. However, there is some disagreement about whether e-commerce will complement or replace traditional bank branches i.e. whether customers will ever feel secure and technically able enough to abandon their local branch for cyberspace. The spokes person for IF (an internet only bank) thinks that there will always be a place in society for the traditional bank, a point we as a group agree with. We also believe that within the next 5 years all transactions and banking processes will be able to be done online.

Another advancement in the future will be a better banking service using the mobile phone. Day by day the mobile becomes more and more advanced. Emailing money is now possible which is convenient for students at university and living away from home. It makes it easier and faster for their families to send them money.

From the predictive commentary above, we can see that the three banks we have chosen are all implementing an e-commerce strategy to some extent. Intelligent Finance, as expected, lead the way, however both Halifax and Bank of Ireland can now boast a very effective Internet presence which complements their offline business. As mentioned earlier, in order to truly realise all of the benefits of e-commerce, it may be required that these banks allow their offline business to be eroded by their online business as the two can conflict. Another reason why Bank of Ireland and Halifax may not be wholly committed to online practices may be that they do not have to be. Intelligent Finance must offer all services online as this is the sector which they predominantly operate in, however if a customer cannot find a service on either the Bank of Ireland or Halifax websites, it is more than likely that a branch is situated nearby who can offer the service to them.

The limitation of e-commerce which is traditionally most often sited is that of security though throughout this report we have mentioned who this problem is eroding by way of fraud guarantees and firewalls (some would say that there was never a security risk associated with the Internet and that it was a myth designed by individuals to scaremonger and keep business transactions offline).

Another problem of e-commerce within the

banking industry is that of global reach. One of the main selling points of

websites is that they can potentially be viewed and used by anyone worldwide.

It is certainly true that the websites we have investigated can be viewed in

many countries, whether they can be usefully used in many countries, however,

is debatable. On www.if.com there is a warning, which reads, This site is intended only for

people who live in the

Bibliography

Afuah, Allan.,

Internet models and strategies: text and cases;

Angehrn, Albert., Designing mature Internet business strategies, European Management journal, 15 (4), 1997, p.361-369.

Begin and Boisvert (2002).

E-commerce: Evaluating the external business environment. CMA Management;

Begin and Boisvert (2002). Strategically deploying e-commerce. CMA Management;

Clarke, N :can internet banking balance the books?(cited 4th November 2002) www.netlondon.com/news/2000-24/518dd5149047fc56802.html

Draenos, S : Round one knockout: Electronic banks vs Bricks and mortar banks, July 2001.

Galliers R.D : Rethinking information systems strategy: Towards an inclusive strategic framework for business information system management.

Good and Schultz

(2002). E-commerce strategies for business-to-business service firms in the

global environment. American Business review;

Guardian online: Banking on assistance(8th may 2002)

Hackbath, Gary and Kettinger, William J., Building an e-business strategy, Information Systems Management, Spring 2000, p. 78-93.

Hickman M , Internet banking : Transactions to active selling: October 1999

Holland C.P and Westwood J.B : Product market and technology: strategies in banking : June 2001 vol 44,no.6.

Intelligent Finance press release (2000) Free internet access will spark an online banking bonanza www.if.com/aboutus/press/20032000.asp

Intelligent Finance press release (2000) customer friendly internet and telephone bank form intelligent finance www.if.com/aboutus/press/18022000.asp

Intelligent finance press release(2000) tele-net banking its all about making the connections www.if.com/aboutus/press/30112000.asp

Intelligent finance press release(2002) chancellor opens new site for UKs number one direct bank www.if.com/aboutus/press/26072002.asp

Malcolm L

Christine (2001). Five e-business strategies you can take to the bank.

Healthcare Financial Management;

Marshall and

McKay (2002) An emergent framework to support

visioning and strategy formulation for electronic commerce. INFOR;

Martin E W et al., Managing Information Technology: What managers need to know, 4th edition, (Chapter 7), Prentice Hall, 2001.

Mols N.P : Organising for the effective introduction of new distribution channels in retail banking 2001

Nour, Mohammed A and Fadlalla, Adam., A framework for Web marketing strategies, Information Systems Management, Spring 2000, p 41-50.

Nsouli, S.M and Schaechter ,A : Challenges of the e-banking revolution : September 2002

Schneider,I :Is time running out for internet only banks: September 2001

Turban, Efraim [et al.]., Electronic commerce : a managerial perspective.

Wenninger, J ; The emerging role of banks in E- commerce :March 2000

Young ,R : The internets place in banking industry: March 2001

General Web sites

www.bank-accounts-online.com

www.epaynews.com

www.qualisteam.com/news/sep02/27-09-02-12.htm

www.usc.edu/dept/annenberg/vol1/issue3/crede.html

www.bankofireland.co.uk

www.abacus-e.com/strat.htm

|

Politica de confidentialitate | Termeni si conditii de utilizare |

Vizualizari: 2173

Importanta: ![]()

Termeni si conditii de utilizare | Contact

© SCRIGROUP 2025 . All rights reserved